The first concern to ask yourself is whether you are willing to initiate your career working in the nonprofit sector complete-big date. If your answer is no, next PSLF isn’t really good for you – and you should believe refinancing your own scientific, dental care, or veterinarian college finance.

While prepared to re-finance, search personal refinancing shortly after you’re making enough currency for aggressive pricing. Overall, greatly with debt students are more inclined to like higher-earnings specialties.

Recall: Very individual lenders give you the most readily useful costs to physicians who have become practicing for quite some time because their rates are derived from your earnings, prior to the level of personal debt you have got. (Panacea Financial’s college student-loan refinancing does not imagine obligations-to-earnings rates as they understand the financial necessary to end up being a doctor.)

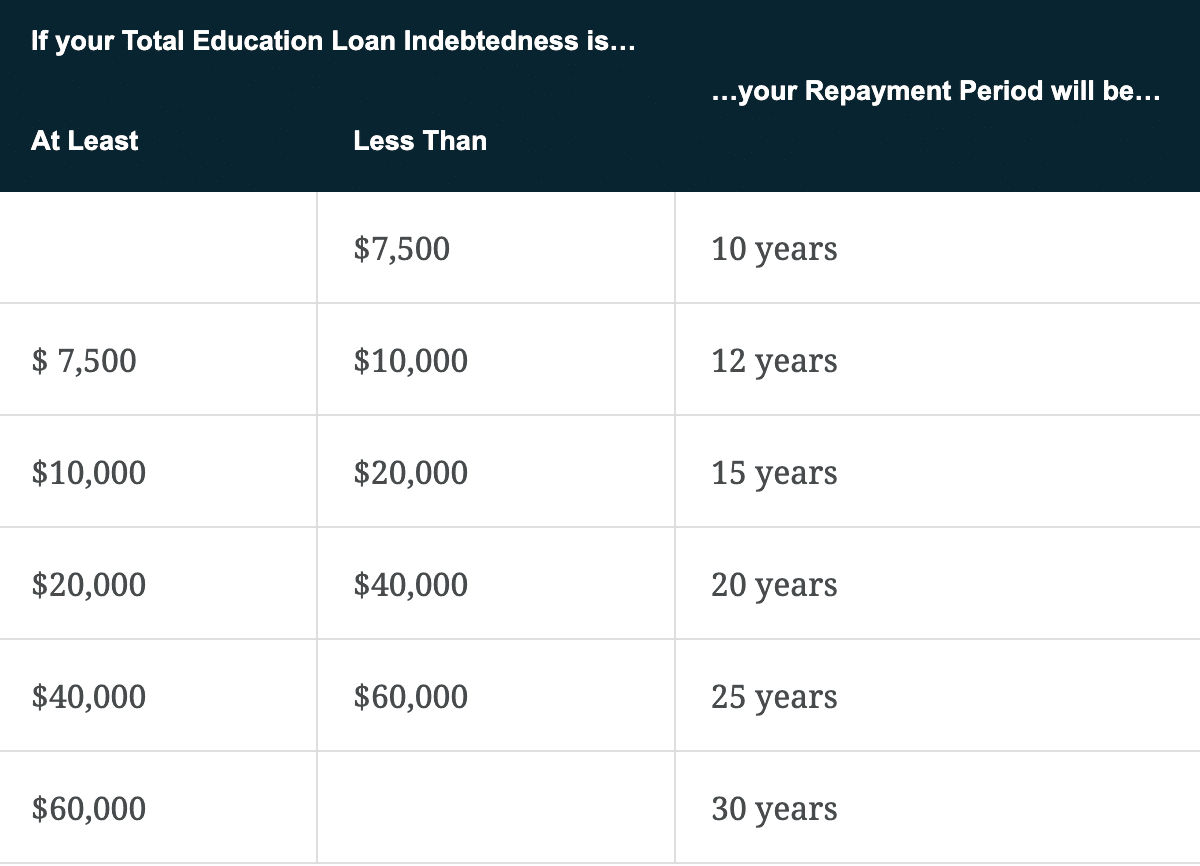

Instead of PSLF, you could follow an effective 20- otherwise twenty-five-12 months forgiveness track, where the bodies writes off of the harmony of federal fund after paying your fund for 20-many years due to a keen IDR. It is possible to still have https://paydayloancolorado.net/bayfield/ to spend fees with this, instead of PSLF, that’s tax-free. (Toward 20-seasons song, the fresh forgiveness number are taxed due to the fact income.)

Out of mention partners doctors are likely to be eligible for brand new expanded forgiveness given that also at a lower life expectancy tier doctor salary, we just make too much. In addition, that it forgiveness isnt tax-free. Because of this on a health care provider ‘ s limited income tax prices, they will certainly are obligated to pay a giant goverment tax bill once they ultimately found forgiveness between 29% and you may fifty% potentially! When you find yourself a health care professional may benefit regarding longer forgiveness option, it should be regarded carefully.

Bear in mind: This is a comparatively new program. No body have done new 20-season requirements at this point, for example there is absolutely no information about just what this whole process is such as.

So if you has actually government money and tend to be committed to full-big date work on a qualifying nonprofit organization, education loan forgiveness is probably a good choice for you

PSLF popularity keeps growing, although program continues to be relatively underutilized. Among medical university graduates opting for top care areas of expertise, 11.7% said they designed to make use of PSLF this season, as compared to 25.3% into the 2014.

Another reason student loan forgiveness might not be most effective for you is when you earn too much money. When you’re there’s no income qualification for PSLF, your own repayment preparations are derived from your income. To determine that it, you will have to calculate your discretionary earnings payments and your ten-season important repayment plan.

In the event your discretionary income money be more than their 10-12 months standard money, you then should consider refinancing. For folks who (or you along with your companion, combined) is actually a leading-earner, you’d be paying the capped ten-season important month-to-month matter. In this situation, you will be making 120 money (10 years) at the ten-12 months important monthly number, and that means you could have paid off an entire amount of brand new financing for example feel forgiven $0. Over that point period, you’ll keeps paid off alot more in attract than simply for folks who got refinanced.

However, the brand new mathematics becomes more complicated if your discretionary payments are almost as much as the ten-12 months simple money. In this situation, you ought to determine the exact desire savings out-of refinancing. In addition may prefer to demand a taxation expert regarding the implications from processing along with your spouse.

Considerations to learn about PSLF

- If you temporarily eliminate qualification, those individuals days only would not matter to your the new 120 collective payments you have to make. In this situation, the brand new costs you already produced still matter on the the complete harmony, and you also do not remove credit towards the forgiveness.

- Youre ineligible having PSLF when you refinance the medical school financing truly.